The cost of retirement is rising: Here’s how to prepare your finances

When you retire, you want to enjoy life free from money worries.

But with the cost of retirement rising, a comfortable lifestyle might be more expensive than you think. In fact, MoneyAge reports that just 9% of working-age people in the UK are currently on track for a comfortable retirement.

By prioritising your retirement savings and creating a comprehensive plan tailored to your needs and circumstances, you can help keep your finances on track to achieve your retirement goals.

Read on to discover how much you could need for a comfortable retirement and learn five steps to help prepare for your ideal lifestyle.

Your costs are likely to evolve throughout your retirement

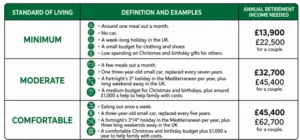

Pensions UK’s Retirement Living Standards indicate how much different retirement lifestyles could cost. The latest figures are based on 2025 prices.

Source: Pensions UK

As suggested above, in 2025, a comfortable retirement cost an average of £45,400 a year for an individual or £62,700 for a couple. However, it isn’t as straightforward as drawing an income at these levels throughout your retirement.

1. Your own costs may vary depending on your lifestyle

Your outgoings in retirement will depend on a range of variables, including where you live. In most cases, you’re unlikely to stick to the exact spending habits outlined above.

2. Your spending habits are likely to change over time

Your lifestyle – and therefore your costs – are likely to evolve throughout retirement.

- Early retirement: To begin with, you may spend more on travelling, socialising, and enjoying active hobbies.

- Mid-retirement: Many people spend less when their energy levels and mobility start declining.

- Late retirement: In later life, your healthcare needs could see your outgoings rise again.

To determine the true cost of your retirement, it’s often wise to consider your ideal and likely lifestyle in each stage.

3. Prices are rising with inflation

The average cost of a comfortable retirement will rise with inflation both before and during your retirement. So, while £45,400 a year may be sufficient for a comfortable retirement in 2025, your retirement income needs are likely to climb as the years go on.

5 steps to prepare for a comfortable retirement

While the cost of a comfortable retirement is rising, that doesn’t necessarily mean it’s out of reach.

Creating a comprehensive retirement plan can help you define, achieve, and enjoy your ideal lifestyle after you stop working. By following these five steps, you could help keep your finances on track for a comfortable retirement.

1. Define your retirement goals

The ideal retirement lifestyle is different for everyone. So, start by visualising what you want out of retirement.

Perhaps you want to travel the world, spend more time with loved ones, or enjoy new and existing hobbies. The Retirement Living Standards could be a good starting point for brainstorming ideas.

Remember to consider how your lifestyle might evolve as your retirement progresses and be realistic about what’s achievable – both financially and physically.

2. Calculate how much your retirement could cost

Once you know how you want your retirement to look, you can start working out how much it’s likely to cost.

Of course, it might not be feasible to pinpoint an exact figure. But with a rough understanding of how much you’re likely to spend each year, you can establish a total target for your pension pot.

It might help to start by reviewing your current expenses and the costs outlined in the Retirement Living Standards. Remember to account for average inflation to project how those costs might rise. These calculations can be complex, so reach out to a financial planner if you would like some support.

3. Prioritise your pension contributions

With a clear view of how much you need to save for retirement, you can plan how you’re going to reach your target.

To help get your savings on track, you might consider prioritising pension contributions. In some cases, this might mean reviewing your budget and making short-term sacrifices to support your long-term goals.

Often, your pot will also benefit from tax relief at your marginal rate (subject to the Annual Allowance), contributions from your employer (for workplace pensions), and growth through your pension’s investment returns.

The earlier you start, the more chance your fund will have to grow.

4. Identify additional income sources

Your private pension might not be your only source of income after you stop working. To get the full picture of your retirement finances, it’s helpful to identify other income sources, such as:

- State Pension payments

- Non-pension savings and investments

- Rental or other property income.

You might also consider whether you plan on downsizing your home, which could release funds to spend in retirement.

A financial planner can help you identify and evaluate all your income sources to understand whether you’re on track to achieve your goals.

5. Plan a sustainable retirement income

The careful planning doesn’t end once you’ve reached your savings target and retired. For a comfortable lifestyle, you’ll need to plan your income to sustain you for the rest of your lifetime.

That way, you can enjoy your retirement without worrying about overspending and running out of money, or underspending and denying yourself things you can afford.

Calculating your retirement income is not always easy. You need to consider your projected expenses (including inflation), your savings’ growth during retirement, and your tax liabilities. Using cashflow modelling to project your outgoings and stress test different variables, a financial planner can help you define a sustainable and suitable income to support you throughout retirement.

Get in touch

Our financial planners can help you define your retirement goals and develop a strategy to stay on track to achieve them. Creating a comprehensive financial plan tailored to you, we can support you in creating a sustainable retirement income that suits your ideal lifestyle.

Email enquiries@jesellars.co.uk or call 01934 875 919 to find out more about how we can help you.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate cashflow planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Workplace pensions are regulated by The Pensions Regulator.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

How can we help?

Have questions about your finances, your future, or unexpected funds? Get in touch for a free, friendly chat.