The 67% tax trap: Why inherited pensions could be taxed twice from 2027

From 6 April 2027, the funds remaining in your pension when you pass away will be included in your estate for Inheritance Tax (IHT) purposes.

In many cases, your pension pot could be taxed twice, with some beneficiaries also being charged Income Tax when they access the funds.

As a result, up to 67% of the funds remaining in your pension when you pass away could go to HMRC, leaving beneficiaries with less than a third of the value.

Keep reading to learn more about why some pensions could be exposed to double taxation from April 2027 and discover six tips for passing on your wealth tax-efficiently.

The new pension rules will push more estates over the nil-rate bands

While your pension will be included in your estate from 6 April 2027, that doesn’t necessarily mean it will be subject to IHT.

IHT is typically charged at 40% and only on the portion of your estate exceeding your nil-rate bands, which are frozen at the following rates until at least 2031:

- Standard nil-rate band: £325,000

- Residence nil-rate band: Up to £175,000 if you leave your primary residence to a direct descendant.

If you’re married or in a civil partnership, you can usually combine your nil-rate bands to pass on a combined total of up to £1 million without triggering an IHT bill. You can leave a pension, as well as any other assets, to your spouse or civil partner without the value being taxed.

Ultimately, including pensions in IHT calculations will push more estates over the nil-rate bands. HMRC estimates that the change will cause 10,500 more estates to become liable for IHT, while 38,500 will face a higher bill.

In certain circumstances, the new rules could also reduce the availability of your residence nil-rate band. The residence nil-rate band tapers down by £1 for every £2 your estate’s value exceeds £2 million. So, if your pension pushes your estate’s value over the £2 million threshold for IHT purposes, your tax liability could rise even further.

Your beneficiaries may be charged Income Tax when accessing your pension

When you draw down from your own pension pot, you can typically take up to 25% as a tax-free lump sum (capped at the £268,275 Lump Sum Allowance, as of 2026/27).

The remaining 75% of your fund is usually subject to Income Tax at your marginal rate.

If you die and leave your pension to a specific person or split it between several people, the Income Tax they pay depends on your age when you pass away, the size of your pension, and their own marginal Income Tax rate.

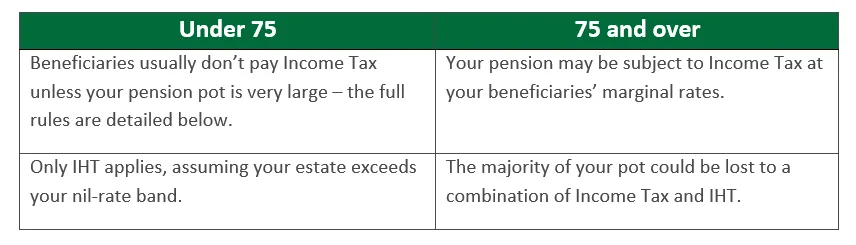

If you die before age 75

The Lump Sum and Death Benefit Allowance (LSDBA) is the total amount that you and your beneficiary can take from your pension pot as lump sums without paying Income Tax.

As of 2026/27, the LSDBA is usually £1,073,100, but may be higher if you applied for protection before 6 April 2025.

The LSDBA includes any tax-free lump sum you withdrew in retirement and funds accessed by your beneficiary, provided they take the money as a lump sum within two years of your death.

If the value of your pension when you die plus the amount taken as a tax-free lump sum during your lifetime is more than the LSDBA, Income Tax may be charged on the portion exceeding the threshold.

If you die after turning 75

Usually, your beneficiary will only be eligible for the LSDBA if you pass away before age 75. If you die aged 75 or older, the total value remaining in your pension pot may be liable for Income Tax.

The rate is determined by the beneficiary’s total annual income, including funds taken from your pension. In some cases, your beneficiary may not have the option to draw down from your pot as a regular income. As a result, they may have to take all the funds remaining in your pension as a lump sum.

Depending on the size of your pot and your beneficiary’s usual income, this could see your pension subject to the additional rate of Income Tax – as well as IHT. As such, it’s important to take proactive steps to avoid falling into this 67% tax trap, including reviewing your existing arrangements and planning to pass on wealth tax-efficiently.

The 67% tax trap: An example

Imagine you pass away at age 85 and leave the £100,000 remaining in your pension to your child. Assuming your other assets use up your full nil-rate band, 40% (£40,000) would go to HMRC as IHT.

Let’s say your child is an additional-rate taxpayer. When they access your pension, the remaining £60,000 will likely attract 45% Income Tax – leaving them with just £33,000 of your £100,000 pot.

In this scenario, 67% of your pot goes to HMRC. If your beneficiary’s income plus your pension fund falls into the basic- or higher-rate tax bands, the rate would be 52% and 64%, respectively.

6 ways to pass on your wealth tax-efficiently

In some cases, a comprehensive financial strategy that aligns both estate and retirement planning could enable you to pass more wealth to your loved ones.

To help mitigate your estate and pension’s IHT and Income Tax liabilities, you might consider:

- Choosing your pension beneficiary carefully. Leaving your pension to a basic-rate taxpayer might mean your pot is charged a lower rate of Income Tax, while naming your spouse or civil partner as beneficiary could remove your pension’s IHT liability. That said, it’s important to carefully weigh the pros and cons of these methods, as they won’t be suitable for all circumstances.

- Planning your retirement income strategically. Carefully considering your drawdown rate can help reduce the amount left in your pot when you pass away, while managing your own Income Tax liability. Once you have withdrawn the funds, you can use the tax-efficient strategies below to mitigate your estate’s exposure to IHT.

- Making financial gifts in your lifetime. Gifting your wealth can help reduce the size of your estate. Financial gifts made up to the gifting allowances (such as the £3,000 annual exemption) and those made more than seven years before your death are typically excluded from your estate for IHT purposes.

- Give regular gifts from your pension. To reduce the size of your pension pot in retirement, you might consider drawing down the maximum amount, while staying within the basic-rate tax band. You could then gift a portion of your income to your loved ones as regular payments – which may exclude them from your estate, subject to strict criteria. You might even opt to make regular contributions to their pension, which would allow them to claim tax relief on your payments at their marginal rate (subject to annual caps).

- Including a charitable donation in your will. Leaving 10% or more of your net estate to charity may reduce your IHT rate to 36%. The value gifted will also be deducted for your estate’s net value, before IHT is calculated, which could help you reclaim any lost residence nil-rate band if your estate is worth more than £2 million.

- Using trusts to reduce your estate’s value. Some trusts can remove assets from your estate, similarly to the gifting rules outlined above. In particular, some people are choosing to take their tax-free lump sum early and place it in trust. The rules for trusts and paying IHT are hugely complex, so it’s worth consulting with a financial planner before placing assets in trust.

It’s important to remember that these steps won’t be suitable for everyone. As such, it’s generally worth speaking with a financial adviser for help in defining a strategy tailored to your unique needs and circumstances.

Learn more: Gifting your wealth in 2026? 4 gifting allowances that could mitigate your tax bill

Get in touch

To find out how we could support you in creating an effective tax-mitigation strategy that works for you and your loved ones, get in touch.

Email enquiries@jesellars.co.uk or call 01934 875 919 to find out more about how we can help you.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning, tax planning, trusts, or will writing.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

How can we help?

Have questions about your finances, your future, or unexpected funds? Get in touch for a free, friendly chat.