7th December 2023

general

Make Pension Contributions

Pension contributions are the simplest way of reducing your higher rate tax liability.

When making personal pension contributions, for every £80 you contribute, basic rate tax relief of £20 is credited directly to your pension. Higher and additional rate taxpayers can then claim extra relief as a reduction in their tax bill.

This must be claimed, so if you don’t already complete a tax return, you should contact HMRC to ensure you are receiving the reliefs you are entitled to. This is only required if you are making the contributions personally. If you are contributing to a workplace pension via salary sacrifice, your payroll department should already be ensuring that you pay the correct tax.

Individuals in the UK have a tax-free personal allowance of £12,570 to set against income. If you are earning over £100,000 per year, the personal allowance is reduced. This results in an effective tax rate of 60% on earnings between £100,000 and £125,140. Making pension contributions can keep your notional earnings below £100,000 so that you retain your personal allowance.

The main advantage of using a pension for tax planning purposes is that the money stays in your hands. You can draw on your pension from age 55 (rising to 57 in 2028), and 25% of the fund value is tax free. You will pay tax on the remaining 75%, but this is usually at a lower rate in retirement. You will also benefit from tax free growth while the pension is invested.

Pensions are also outside your estate for Inheritance Tax purposes, providing a secondary tax benefit.

You can make gross pension contributions up to the level of your relevant earnings, for example, salary or business profits. This is further capped by the annual allowance of £60,000, however you may be able to carry some of this forward from previous years. Your annual allowance will be reduced if you earn over £240,000 or if you have already flexibly accessed your pension.

You can find out more here. You may also want to seek financial advice if you are thinking about making substantial pension contributions.

Optimise Tax Free Allowances

Higher rate taxpayers can benefit from the following allowances:

Use Your ISA Allowance

You can contribute up to £20,000 to your ISA.

Making ISA contributions won’t have an immediate impact on your tax bill. However, all income and growth is tax-free and you can make withdrawals at any time without tax or penalty. ISAs are a useful component of a long-term tax planning strategy.

If you take a withdrawal, you can replace the funds in the same tax year and retain your full annual ISA allowance as long as the provider allows this.

ISAs can also be transferred to a spouse on death, without using up any of their allowance.

Buy Company Shares

If your employer runs a recognised share scheme, it can be worth making use of this. Your contributions will be deducted from your salary and are not subject to tax or National Insurance.

There could also be other advantages, for example the ability to buy shares at a pre-agreed price, which may be below market value.

There are a number of different schemes available. Normally there is a requirement to hold the shares for a minimum period before selling.

Capital gains tax may be payable on eventual sale once the shares have vested.

Remember to read the scheme details carefully. Shares are a higher risk investment, so should only form a small part of your investment strategy.

There is also the question of whether your company is a good investment. If you have doubts about your employer’s financial strength, you may wish to consider the risk you are taking simply by working there.

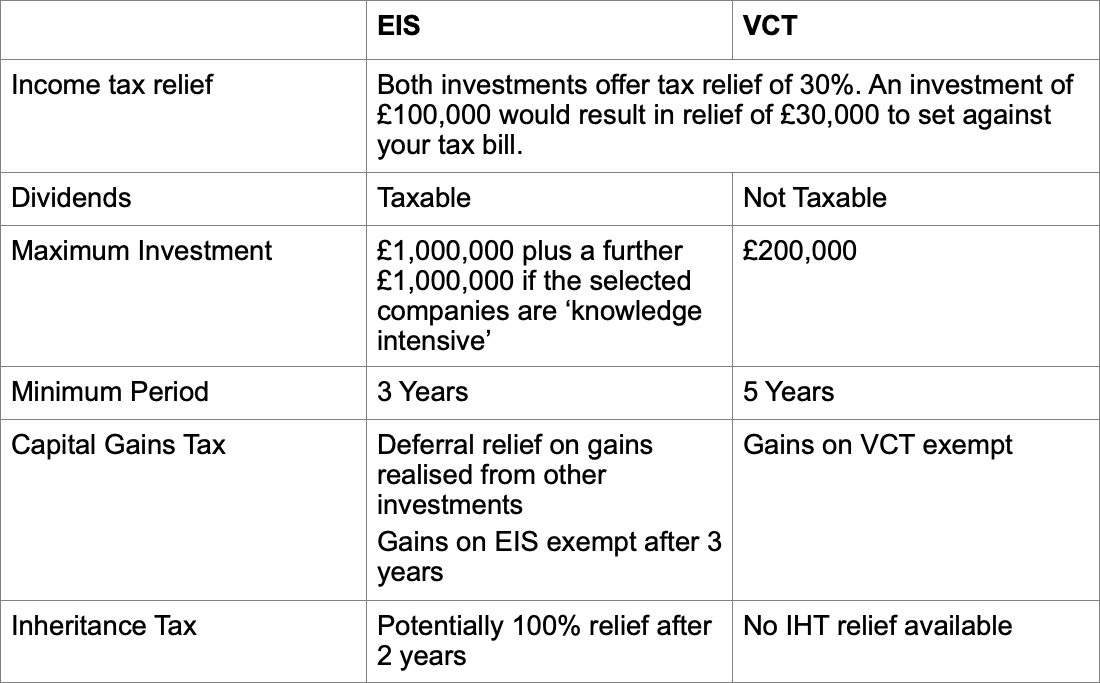

Tax Advantaged Investments

After you have used your pension and ISA allowances, you might want to consider an Enterprise Investment Scheme (EIS) or Venture Capital Trust (VCT) for some of your surplus.

These are high risk vehicles for investing in smaller companies. You should only consider these investments if you can afford to lose the money. The investment must be held for a minimum period (3 and 5 years respectively) to retain the tax relief.

Of course, there is potential for significant growth as well as substantial tax benefits. The main implications are summarised below:

While EIS and VCT investments can form part of a financial planning strategy, they are not suitable for most investors. Advice is recommended.

Tax planning is not the most important part of a financial plan, and should not unduly influence your investment decisions. However, there are several ways of reducing your higher rate tax liability that will also complement your overall financial strategy.

Please do not hesitate to contact a member of the team if you would like to find out more.